Singapore's New IP Rider Rules (April 2026): What the Co-Payment Change Actually Means for Your Hospital Bill

New MAS/MOH IP rider rules kicked in April 2026. Full-rider coverage where your insurer picks up 100% of your hospital bill is gone. Here is a plain-English breakdown of mandatory co-payments, who is most affected, and what to do next.

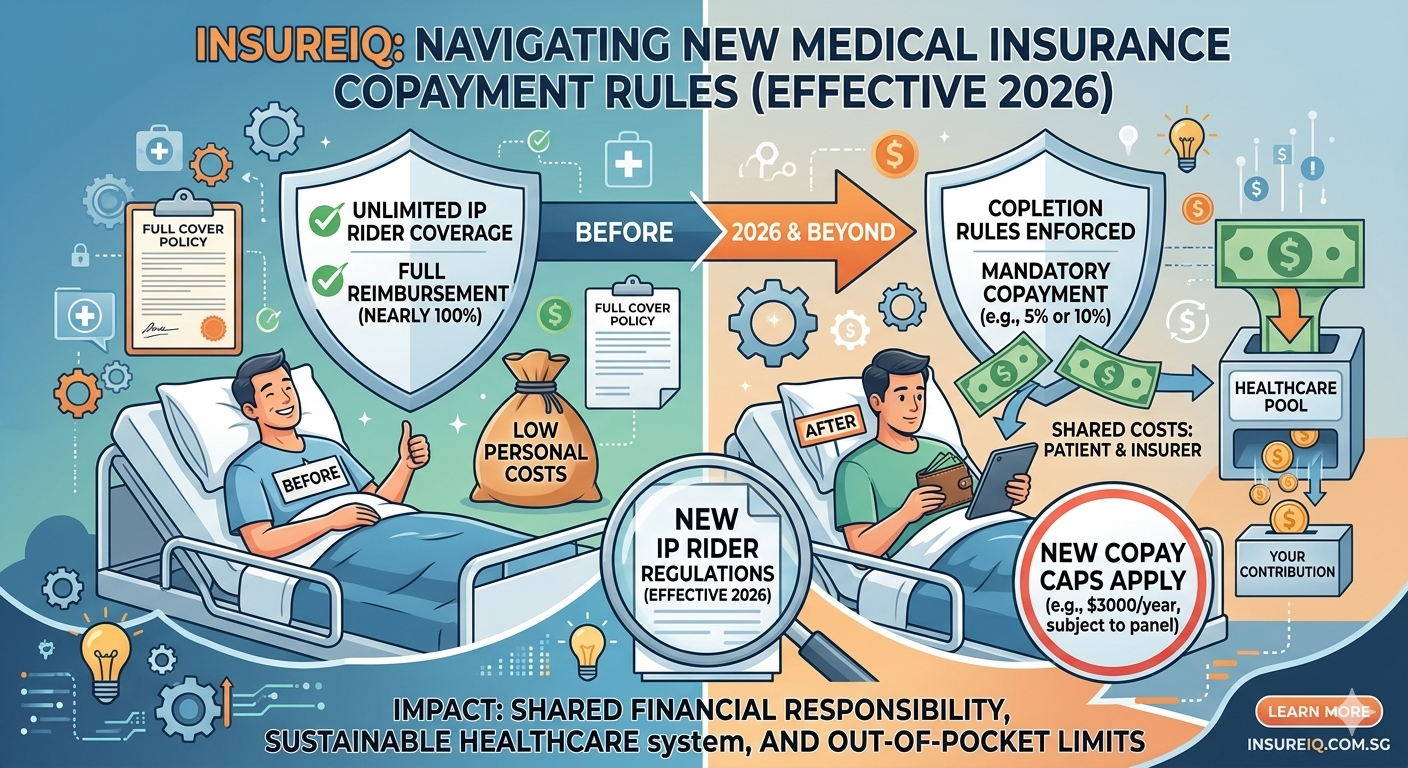

What Is an IP Rider, and Why Does It Matter?

Let's start at the beginning. Every Singapore Citizen and Permanent Resident is enrolled in MediShield Life, a basic national health insurance plan that covers large hospitalisation bills — but only up to Class B2/C ward limits in public hospitals.

An Integrated Shield Plan (IP) tops up MediShield Life to cover Class A/B1 wards in public hospitals, or private hospital stays. Insurers like AIA, Singlife, NTUC Income, Prudential, and Great Eastern offer these plans.

An IP rider is an add-on to your IP that covers the portions your IP itself doesn't — things like deductibles, co-insurance, and other out-of-pocket costs. Until April 2026, many riders offered near-total coverage, meaning policyholders could be hospitalised and walk out paying almost nothing.

That's the part that has now changed.

What Exactly Changed in April 2026?

Effective 1 April 2026, MOH introduced two significant changes to all new and renewed IP riders:

Change 1 — Co-payment cap raised to S$6,000 The minimum 5% co-payment requirement that has existed since 2018 remains unchanged. However, the annual cap on that co-payment has been raised from S$3,000 to S$6,000 per policy year. This means your maximum co-payment exposure has doubled.

Change 2 — Riders can no longer cover the minimum IP deductible This is the bigger change. Previously, riders could cover your deductible entirely. From April 2026, new riders cannot cover the minimum IP deductible set by MOH. These deductibles vary by ward class:

| Ward Type | Minimum Annual Deductible |

|---|---|

| Class A / Private Hospital | S$3,500 |

| Class B1 | S$2,500 |

| Class B2 | S$2,000 |

| Class C | S$1,500 |

| Day Surgery / Short Stay (non-subsidised) | S$2,000 |

| Day Surgery / Short Stay (subsidised) | S$1,500 |

These deductibles can be paid using MediSave, subject to prevailing withdrawal limits.

The upside: New rider premiums are expected to be approximately 30% lower than existing maximum coverage riders, reflecting the reduced scope of coverage.

This applies to all riders sold or renewed from 1 April 2026 onwards. Existing riders will be subject to the new rules upon renewal.

The stated rationale from MOH: to reduce over-utilisation of private healthcare and slow the medical cost inflation that has made premiums increasingly unaffordable for ordinary Singaporeans.

A Real-Money Example: Your S$20,000 Hospital Bill, Before and After

Let's say you're warded in a Class A ward for a procedure totalling S$20,000.

Under the Old Rules (Pre-April 2026, Full Rider)

| Item | Amount |

|---|---|

| Total bill | S$20,000 |

| Covered by MediShield Life | S$2,000 |

| Covered by IP plan | S$15,000 |

| Covered by rider (deductible + co-insurance) | S$3,000 |

| Your out-of-pocket cost | S$0 |

Under the New Rules (Post-April 2026)

| Item | Amount |

|---|---|

| Total bill | S$20,000 |

| Covered by MediShield Life | S$2,000 |

| Covered by IP plan | S$15,000 |

| Minimum deductible (rider cannot cover this) | S$2,500 (Class B1) / S$3,500 (Class A/Private) |

| 5% co-payment on remainder (capped at S$6,000/year) | ~S$500 |

| Your minimum out-of-pocket cost | S$3,000–S$4,000 |

Your actual out-of-pocket cost under the new rules has two components that stack: the uncoverable deductible (S$1,500–S$3,500 depending on ward) plus the 5% co-payment on the remaining amount, capped at S$6,000 per year. The deductible portion can be paid via MediSave.

Who Is Most Affected?

Not everyone feels this equally. Here's a quick guide:

Most affected:

- Policyholders with full riders on Class A or private hospital plans — the uncoverable deductible is S$3,500, on top of the 5% co-payment

- Frequent hospitalisers — those with chronic conditions who make multiple claims per year are more likely to pay the full $6,000 co-payment cap, which is double the previous $3,000 limit.

- Seniors whose premiums are already high and who now face additional mandatory out-of-pocket costs

Less affected:

- Policyholders on Class B2 or C plans — the minimum deductible is S$1,500–S$2,000, and the 5% co-payment on subsidised ward bills is modest

- Those who rarely make claims — the deductible and cap mean your maximum exposure is fixed and predictable

- New policyholders — their premiums will be approximately 30% lower under the new rider structure

What Should You Do Right Now?

Here are four practical steps:

-

Check your rider renewal date. If it falls after 1 April 2026, the new co-payment rules will apply at renewal. Contact your insurer or check your policy documents.

-

Calculate your real out-of-pocket exposure. Use the cap figures (S$3,000 for public hospital plans, S$5,000 for private) to understand your worst-case annual cost. Can you absorb that from savings?

-

Compare your options before auto-renewing. Don't simply accept the renewed premium without shopping around. Different insurers price their riders differently, and the panel of covered hospitals also varies.

-

Use MediSave for your deductible. The mandatory minimum deductible (S$1,500–S$3,500) that your rider can no longer cover can be paid from MediSave, subject to prevailing withdrawal limits. Make sure your MediSave balance is sufficient to absorb this cost.

The Bottom Line

The April 2026 IP rider changes are significant, but they don't have to be stressful — if you understand what's changed and make an informed decision. The era of zero-cost hospitalisation is over, but the new co-payment structure is capped and predictable. For most Singaporeans, keeping a rider (even under the new rules) still offers meaningful financial protection against the rising cost of private healthcare.

What matters most is that you review your existing plan, understand your new exposure, and compare your options with clear eyes.

Compare Integrated Shield Plans and riders side by side at insureiq.com.sg — no agent required.

Terms and conditions apply. Premium figures and co-payment caps referenced are based on MOH/MAS guidelines. Individual plan details vary by insurer. This article is for informational purposes only and does not constitute financial advice.

Get the next article

New articles on Singapore insurance policy gaps, claim denials, and regulatory changes — delivered to your inbox when published. No spam, no weekly digest.

Free. Unsubscribe any time. InsureIQ will not share your email.