Your Critical Illness Policy Might Not Cover the Illness That Kills You

A Singaporean paid premiums for years. His insurer said the tumour was not life-threatening enough. He got nothing. Medicine has moved on — most CI policies have not. Here is what that gap costs policyholders and what you can do before you file a claim.

Singapore's Critical Illness Gap Is Not a Fringe Problem

Around the same time, a thread appeared on Reddit's r/singapore with a simple, exhausted title: "Done dirty by Singlife." A policyholder described a cancer-related CI claim being rejected under their Singlife MultiPay CI policy. The post resonated immediately — upvotes, shares, and comment after comment from Singaporeans who recognised the pattern or feared they were in the same position without knowing it.

The community's verdict was blunt: "pls check if you have this Singlife MultiPay CI policy. if suay might end up in the same situation."

One commenter put it plainly: "LIA encourages insurers to update their policies whenever definitions change and inform their policyholders — but other companies are doing the same, ignoring LIA's lip service."

That observation cuts to the heart of the problem.

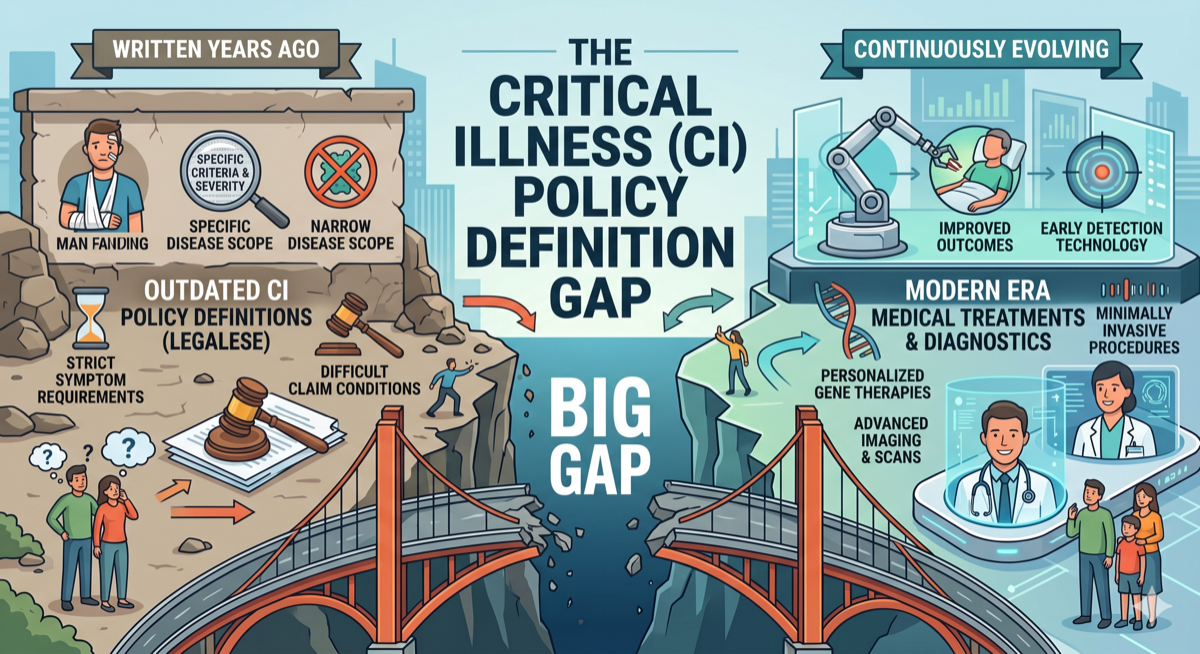

How Singapore's CI Framework Got Left Behind

The Life Insurance Association of Singapore (LIA) publishes standardised definitions for 37 critical illness conditions. These definitions — the literal words that determine whether your claim is paid — have been updated just four times in the history of CI insurance in Singapore: before 2003, in 2003, in 2014, and in 2019.

The 2019 framework became the industry standard. It remained so for six years.

Six years during which:

- Liquid biopsies became capable of detecting cancers years before they become symptomatic

- High-sensitivity troponin tests redefined what constitutes a "heart attack"

- Keyhole cardiac procedures replaced open-chest surgery as the standard of care

- Immunotherapy converted previously terminal diagnoses into manageable chronic conditions

In May 2025, LIA finally announced the CI Framework 2024 — the first meaningful update in six years — with an implementation deadline of 1 October 2025. The changes were framed explicitly as aligning definitions "with advances in medical technology" to reduce "ambiguity for policyholders making claims."

Read that again: the industry's own regulator acknowledged, in writing, that the existing definitions created ambiguity for policyholders making claims.

What Actually Changed — and What It Reveals About What Was Wrong Before

The 2024 framework updates are instructive not just for what they add, but for what their existence admits about the old definitions. Here are some of the changes:

Open-Heart Valve Surgery — Previously, many policies required literal opening of the chest wall. The 2024 framework now accepts "an incision on the heart for direct visual replacement or repair" — but critically, still excludes keyhole and catheterization procedures. This means minimally invasive valve surgery, now the dominant approach in Singapore's cardiac centres, may still fall outside coverage depending on how your specific policy is worded.

Heart Attack — The definition of "Other Serious Coronary Artery Disease" was revised to provide "clearer understanding of the real intention and requirements." In plain English: the old definition was unclear enough that insurers and policyholders interpreted it differently. Policyholders lost those disputes.

Cancer — Updated to reflect the WHO's 2022 reclassification of pituitary neuroendocrine tumours (PitNET) as a distinct entity. The fact that a definitional update had to track a 2022 WHO taxonomy change that took until 2025 to implement illustrates the lag precisely.

Deafness — Now defined with a specific decibel threshold (80dB or greater across all frequencies). Before this, "total" hearing loss was vague enough to dispute.

Every one of these changes represents a category where, under the old framework, a legitimate claim could be — and was — denied.

The Catch: Your Old Policy Does Not Automatically Update

This is the critical detail most Singaporeans holding CI policies do not know.

The 2024 framework mandates that new policies issued from 1 October 2025 must use the updated definitions. It does not automatically update existing policies.

The LIA "encourages" insurers to migrate existing policyholders to updated definitions and notify them of changes. Encouragement is not obligation. Some insurers are treating LIA encouragement as exactly that — optional.

If you bought your CI policy in 2018, 2020, or even 2023, you may still be governed by definitions that the industry itself has now publicly acknowledged needed updating. Nobody is required to tell you. Many will not.

Parliament has taken notice. Written parliamentary questions have been raised on the government's monitoring of insurance claim denials and the number of complaints MAS has received regarding disputed claims — a signal that this is no longer just a consumer advocacy issue.

You Are Paying Today's Premiums for Yesterday's Definitions

A standard whole-life CI policy in Singapore covering S$200,000 might cost S$300–500 per month depending on age and sum assured. Over 20 years, that is S$72,000–120,000 in premiums paid.

A claim rejection does not mean you lose the premium money — you have already spent that. What you lose is the entire financial purpose of having the policy: the lump sum that was supposed to cover treatment costs, lost income, home modifications, and the gap between what MediShield pays and what a serious illness actually costs.

In Singapore, cancer treatment at a private hospital can run to S$200,000 or more for surgery, chemotherapy, and follow-up. A single stroke hospitalisation with rehabilitation can exceed S$50,000. These are the exact scenarios CI insurance exists to address — and the exact scenarios where a definitional mismatch leaves policyholders with nothing.

A Mothership report from October 2025 documented a Singaporean whose S$100,000 AIA claim for a benign brain tumour was denied because the insurer deemed the condition "not life-threatening" at the time of surgery — even though current LIA definitions do not require a benign brain tumour to be life-threatening to qualify. His policy was written under older definitions. Nobody told him.

The AIA brain tumour claimant did not lose S$100,000 when his claim was denied. He never had it. He just did not know until he needed it.

The Cruel Irony of Modern Medicine

The deeper problem runs in a direction most policyholders never consider.

Catching cancer early is the entire goal of modern screening. Early-stage detection saves lives, reduces treatment intensity, and cuts long-term healthcare costs. Singapore actively funds screening programmes for this reason.

But many CI policies still exclude early-stage cancers, carcinoma in situ, and low-grade malignancies — because those conditions were not considered "critical" when the policy definitions were written.

The better your doctor is at detecting disease early, the less likely your CI claim is to be approved.

The same logic applies to cardiac care. Keyhole valve repair has lower complication rates, faster recovery, and better long-term outcomes than open-chest surgery. Surgeons choose it precisely because it is safer for the patient. But if your policy requires open-chest surgery to trigger the benefit, the better your hospital treats you, the weaker your claim.

This is not a corner case. This is a structural misalignment between the incentives of modern medicine and the frozen definitions of legacy insurance contracts.

Knowing Where You Stand Is Now a Basic Requirement

The problem is not that Singaporeans are uninsured. Most financially literate Singaporeans have at least one CI policy, often more. The problem is that coverage on paper and coverage in practice have diverged — and the divergence is invisible until a claim is filed.

Knowing your coverage position requires answering questions most policy documents do not make easy:

- Does your CI policy use 2019 definitions or 2024 definitions?

- For cancer — does your policy cover early-stage diagnoses, or only invasive malignancies?

- For cardiac events — what troponin threshold triggers your policy's definition of heart attack?

- For surgical procedures — does your policy pay for keyhole cardiac surgery, or only open-chest?

- If you hold multiple CI policies, do they stack, or do their exclusions compound?

These questions require reading the actual policy language — not the product brochure, not the sales illustration, not a summary page.

The LIA Definition Gap: Real Cases, Real Money Lost

The gap between what the LIA framework says and what older policies actually cover is not theoretical. It has cost Singaporeans real money:

- S$108,500 denied — Prudential, brain aneurysm: A woman who suffered a ruptured brain aneurysm had her claim rejected because her 2016 policy required open-skull craniotomy. Her surgeon performed a modern endovascular repair instead. Same condition, different technique — claim denied. She is now suing Prudential in the State Courts.

- S$100,000 denied — AIA, benign brain tumour: A policyholder's claim was rejected on the basis that his tumour was "not life-threatening" at the time of surgery — a requirement that does not exist under current LIA definitions. His policy predated the updated framework.

- Cancer CI claims rejected — Singlife MultiPay: A Reddit r/singapore thread titled "Done dirty by Singlife" went viral after a policyholder's cancer-related CI claim was rejected under a MultiPay policy. Community response was immediate: dozens of others reported holding the same policy with no idea whether their coverage would hold.

In each case, the policyholder did nothing wrong. They paid their premiums. The definitions their policies were written against simply did not keep up with how medicine and surgery evolved.

This Is What InsureIQ Does

InsureIQ is an AI-powered platform built specifically for the Singapore market that reads your actual policy documents and tells you where you stand — before you ever need to file a claim.

Upload your CI policy and InsureIQ will:

- Run a LIA compliance check — identifying whether your definitions meet 2024 standards or fall below them, flagging conditions where your policy language is more restrictive than current minimums

- Map your specific definitions for cancer, heart attack, stroke, and other covered conditions against what modern medicine is actually treating and detecting

- Identify coverage gaps — specifically the scenarios where your policy may not respond: early-stage cancers, minimally invasive procedures, modern cardiac diagnostics

- Analyse multiple policies together — if you hold policies from different insurers, InsureIQ maps how they interact and where gaps compound rather than cancel

- Generate plain-English scenario analysis — what would happen to your claim today if you were diagnosed with an early-stage thyroid cancer, or required keyhole valve repair, based on your actual policy wording

The man who was told his brain tumour was not "life-threatening enough" did not know there was a problem with his coverage until he was in a hospital bed. That is the worst time to discover a gap.

Start your free LIA compliance check at InsureIQ — because the policy you believe you have and the policy you actually have may not be the same thing. Find out now, while you still have time to fix it.

Get the next article

New articles on Singapore insurance policy gaps, claim denials, and regulatory changes — delivered to your inbox when published. No spam, no weekly digest.

Free. Unsubscribe any time. InsureIQ will not share your email.