A $108,500 Brain Aneurysm Claim Was Denied: What Outdated Surgical Definitions Mean for Your Policy

A Singapore woman had her $108,500 brain surgery claim denied because her 2016 policy required open-skull surgery — but her surgeon performed a modern minimally invasive procedure. Here is what this case reveals about the definition gap in Singapore critical illness policies.

When a Brain Aneurysm Claim Gets Denied: The Surgical Definition Problem

You pay your premiums every month. You trust that when something goes wrong, your insurer pays. Then the worst happens — and you find out the protection you thought you had does not exist.

That is the story of Cai Yanhong, 45, who suffered a ruptured brain aneurysm in 2023, collapsed on a bus, and woke up in the ICU. She recovered. Then her insurer denied her $108,500 critical illness claim. The reason: a single clause that defined her surgery in a way that had not kept up with modern medicine.

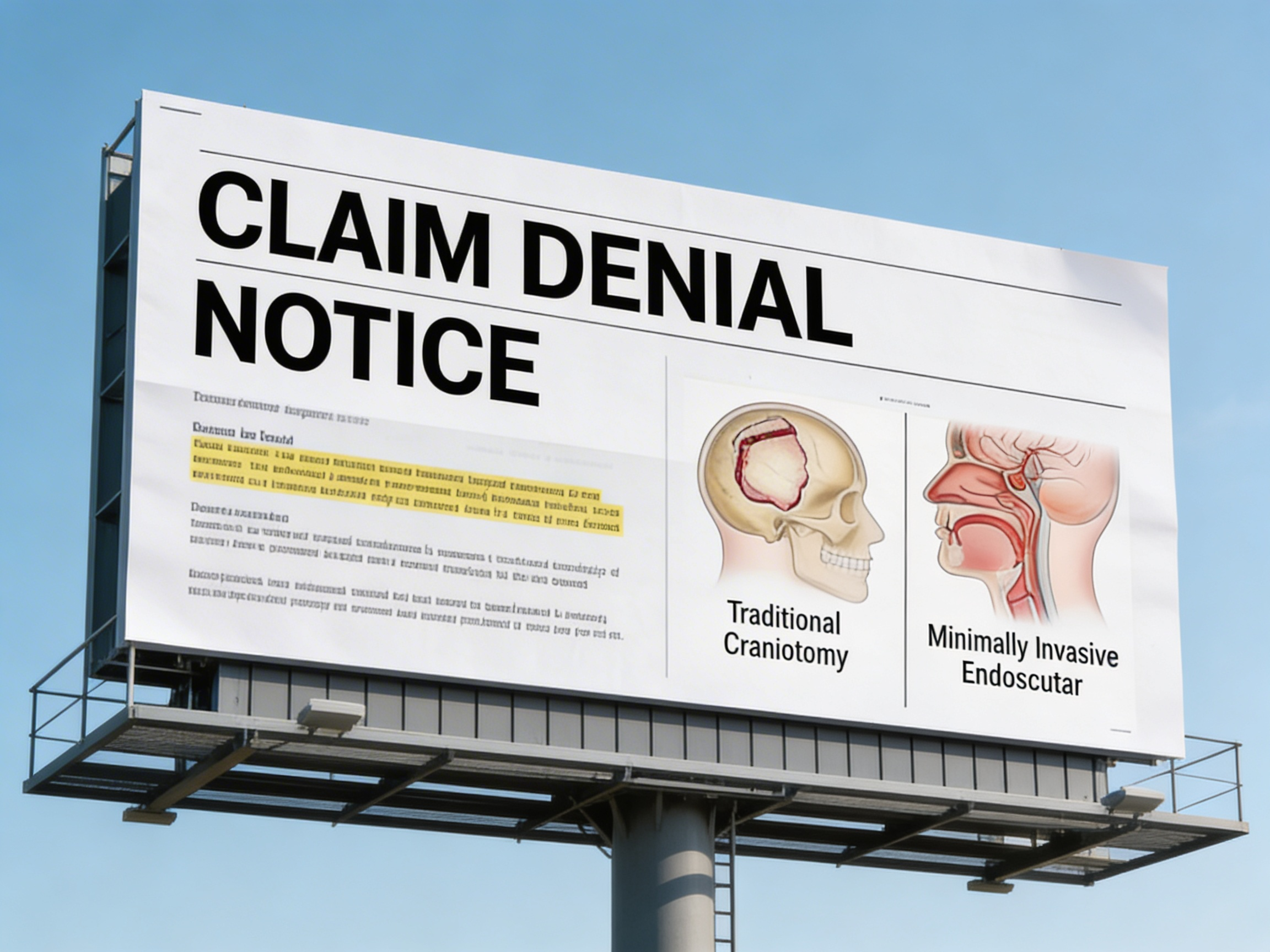

How Can an Insurer Deny a Brain Aneurysm Claim?

The policy only covered brain aneurysm surgery performed via surgical craniotomy — an open-skull procedure. Her surgeon performed an endovascular repair instead, which is the standard minimally invasive treatment used in hospitals today.

She was unconscious when the surgical decision was made. She had no choice in the procedure used. The policy she bought in 2016 used definitions from that era. By 2023, medicine had moved on. Her insurer had not updated the definition. Nobody told her.

She is now suing her insurer in the State Courts, representing herself.

Does Your Policy Cover Minimally Invasive Surgery? How to Check

Most Singapore critical illness policies purchased before 2020 define surgical procedures using outdated methods. If your policy was incepted under the LIA 2003 or 2014 framework, your surgical definitions may not reflect modern clinical practice.

When you upload your policy to InsureIQ, the LIA compliance checker compares your policy's definitions against the current LIA CI Framework standards. It checks whether your policy covers a condition based on diagnosis alone, or whether it requires a specific surgical method.

If Cai had uploaded her policy before her aneurysm, InsureIQ would have flagged it: this policy requires surgical craniotomy. Endovascular procedures are excluded.

That is not financial advice. It is a factual translation of what her policy said versus what the LIA standard says.

The Same Condition, Two Different Insurers — Two Different Outcomes

A second woman came forward after Cai's case was reported. She held policies with two different insurers, suffered five brain aneurysms, and submitted identical documents to both. One insurer paid immediately. The other denied it — same condition, same treatment, two completely different outcomes.

Different insurers use different definitions. This is the definition gap: the space between what your doctor calls your condition and what your policy contract requires. InsureIQ cannot tell you which policy is better. But it can show you exactly what your policy says before a claim event, not after.

Key questions to ask about your own policy:

- Does your policy specify a surgical method for neurological conditions?

- Was your policy incepted before 2020, when the LIA framework was last updated?

- Has your insurer issued any endorsements updating surgical definitions since your policy was issued?

How to Protect Yourself Before You Need to Claim

Upload your policy to InsureIQ and ask: "Does my brain aneurysm benefit require a specific type of surgery?" InsureIQ will find the clause, explain what it means, and flag whether it matches current LIA standards.

Cai needed that information in 2022. Not in September 2023, when the claim letter arrived.

Upload your policy and ask your first question free. No sign-up required.

Get the next article

New articles on Singapore insurance policy gaps, claim denials, and regulatory changes — delivered to your inbox when published. No spam, no weekly digest.

Free. Unsubscribe any time. InsureIQ will not share your email.